Method - Calculator for determining the shares of net profit of partners in a joint business

Optimize your partnership cooperation with our protected proprietary method of calculating net profit shares. The principle of fairness and flexibility to change conditions ensures the stability and development of your business

The method of determining the shares of net profit is based on the analysis and periodic assessment of key business factors:

I – authorship of a business idea or model.

M – investment of working capital.

F – use of fixed and intangible assets.

mm – participation in creative management.

R – uninsurable risks.

Each factor is assessed in percentage points, where I has a maximum of 10, and M, F, mm and R – up to 50 points. The partners agree on the contribution and recalculate it into a share of net profit. The method also takes into account changes in the composition and roles of the partners.

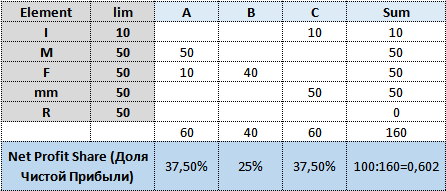

Example:

Let’s look at an example: partners A, B and C open a shoe repair shop. C is the author of the idea and the manager, B provides the premises, A — equipment and funds. The shares are determined:

Want to know how our method can optimize your business?

Leave a request for a consultation and get an individual assessment.

Payment

Payment for the consultation is voluntary according to the next pay system: you pay for the consultation for the next client after a positive result in solving your issue.

The cost is either €10 plus a short review, or €30 one-time.

Availability of paid consultations:

Customer Reviews

Dmitry К.

This method allowed us to avoid many conflicts and misunderstandings among partners. Now everyone has a clear understanding of their share and contribution to the common cause.

Elena P.

We have successfully implemented the method in our business and the results have exceeded expectations. The method really makes the distribution of profits transparent and fair.

Вопросы и ответы

How often should partners' shares be recalculated?

It is recommended that a recalculation be carried out when there are significant changes in the business, such as a change in the composition of partners, a significant change in elements or shares of participation, and also before each new division of profits.

Is the method suitable for all types of business?

Yes, the method is flexible and can be adapted to various business models, including startups, small and medium businesses, and large enterprises.

How does the consultation process work?

The consultation includes an analysis of your business model, an assessment of the factors and the development of a profit distribution scheme. We provide detailed recommendations and explanations.

What is the cost of a consultation?

Payment for the consultation is voluntary according to the next pay system: you pay for the consultation to the next client after a positive result in solving your issue. The cost is either €10

plus a short review, or €30 one-time.

What guarantees are there for the effectiveness of this method?

The method has been tested successfully and has proven itself as a reliable way to ensure fair distribution of profits. We use proven practical cases to demonstrate its effectiveness.